The Weekend Rip

Happy Weekend!

Markets capped a wild week with a 3% gain as a fragile two-week ceasefire in the Middle East triggered a massive relief rally, overcoming a terrifying 1% monthly inflation spike and record-low consumer sentiment. While the energy trade unwound and oil dipped below $100, the tech sector surged on record Taiwan Semiconductor Manufacturing Company revenues and massive infrastructure deals for Anthropic’s new model. Investors are now balancing geopolitical optimism against the Fed's new anxiety over AI-driven systemic risks and a "hot" CPI print that refuses to cool.

Let's recap and prep you for the week ahead. 📝

Monday 🕊️: Markets climbed broadly as investors weighed Trump's ultimatum to Iran against ceasefire optimism, with oil names and travel stocks catching a bid on strait-reopening hopes. The managed care sector was the day's standout, surging after CMS finalized a 2.48% Medicare Advantage rate increase for 2027, well above what Wall Street had braced for and worth $13 billion in additional payments to insurers. Jamie Dimon dropped his annual shareholder letter warning of stagflation, overleveraged households, and cracks in private credit, which is either required reading or the most expensive thing you'll ignore this week.

Tuesday 🌋: Markets buckled under apocalyptic war rhetoric and an overnight oil spike, then steadied as Oman‑brokered shipping talks surfaced and ceasefire hope crept back into the tape. Energy and defense were the only clean winners early, but the day ended with a hesitant grind higher as investors clung to any signal the Hormuz choke could ease. After hours, deal and policy headlines carried the tape — Ackman’s UMG relisting pitch, Paramount’s sovereign‑capital lifeline, Broadcom’s expanded AI chip pipeline, and a surprise Medicare Advantage rate bump that lifted healthcare.

⚡Wednesday: Markets ripped on a Pakistan‑brokered two‑week ceasefire, with oil sliding below $100 and a full‑throttle risk‑on rotation into semis, industrials, travel, and cyclicals while energy got smoked. The relief rally was violent and broad, but still fragile given the short fuse and ongoing regional risk, so traders treated it like a reprieve, not a resolution. Earnings and single‑stock moves took a back seat to the ceasefire tape, though Delta’s strong quarter and Meta’s AI model launch added fuel to the rally’s tech/consumer tilt.

Thursday 🥶: Markets stayed green on ceasefire relief, but the tape snapped back to the other storylines we shelved during the oil shock: SaaS multiples got hit hard, AI margin fears returned, and macro inflation data stayed sticky. Oil stalled while the Strait remained mostly closed, leaving energy weaker and software in free‑fall even as broader indexes held up. Consumer data was mixed, and Artemis II’s imminent splashdown added a rare non‑market headline to a day dominated by rotation and sector pain.

Friday 🕊️: Markets closed a volatile week on a high note as an Iran ceasefire announcement sparked a relief rally, though Friday saw a slight cooling following a massive 1% monthly spike in inflation driven by surging gas prices. While consumer sentiment hit all-time lows, the tech sector remained resilient with Taiwan Semiconductor Manufacturing Company posting record revenues and Anthropic’s new "Mythos" AI model triggering emergency cybersecurity briefings between the Fed and major banks. Despite the macro tension, investors are cheering a 3% weekly gain for the major indexes as diplomatic talks begin.

🤩 This week's Stocktwits Top 25 showed how momentum movers fared vs. the indexes. Also the talks did not go that well, and the U.S. is now ‘blockading’ the Strait of Hormuz.

Here are the closing prices:

Ticker | Asset Class / Sector | WTD % Change | YTD % Change |

SPY | S&P 500 (Broad Market) | +3.56% | +8.20% |

QQQ | Nasdaq-100 (Tech/Growth) | +4.68% | +12.45% |

DIA | Dow Jones Industrial Average | +3.50% | +4.10% |

XLB | Materials Select Sector | -0.15% | +2.15% |

XLV | Healthcare Select Sector | +0.34% | +1.80% |

THE BRIEF

Need a concise summary of what's going on this week? Look no further. Here’s a rundown of this week’s earnings and economic data.

Earnings This Week

Above is a quick summary. Check out the full Stocktwits earnings calendar for the other names reporting this week.

Week of April 13, 2026

Pre-Market Earnings

Mon: $KINI, $GS Goldman Sachs, $IVDA Iveda Solutions Inc, $FAST Fastenal

Tue: $JPM JPMorgan Chase, $WFC Wells Fargo, $JNJ Johnson & Johnson, $C Citigroup, +5 more

Wed: $BAC Bank of America, $MS Morgan Stanley, $PNC PNC Financial Services

Thu: $PEP PepsiCo, $SCHW Charles Schwab Corporation, $JKS JinkoSolar Holding Co LTD, $USB U.S. Bancorp, +5 more

Fri: $ERIC, $ALLY Ally Financial Inc

After-Market Earnings

Mon: $ZENA, $XTIA XTI Aerospace Inc., $OZSC Ozop Energy Solutions, $DPLS Dark Pulse Inc, +27 more

Tue: $BMNR, $SPWR, $STI Solidion Technology Inc, $MSPR MSP Recovery Inc - Ordinary Shares - Class A, +3 more

Wed: $KMI, $MAXN, $GPUS Hyperscale Data Inc., $ARAI Arrive AI Inc

Thu: $NFLX Netflix, $SNAP Snap Inc, $AA Alcoa Corp, $LAKE Lakeland Industries Inc, +1 more

Fri: $AIRE reAlpha Tech Corp., $RF Regions Financial Corporation, $TFC Truist Financial, $FITB Fifth Third Bancorp

Economic Calendar

In addition to the above, check out this week's complete list of economic releases.

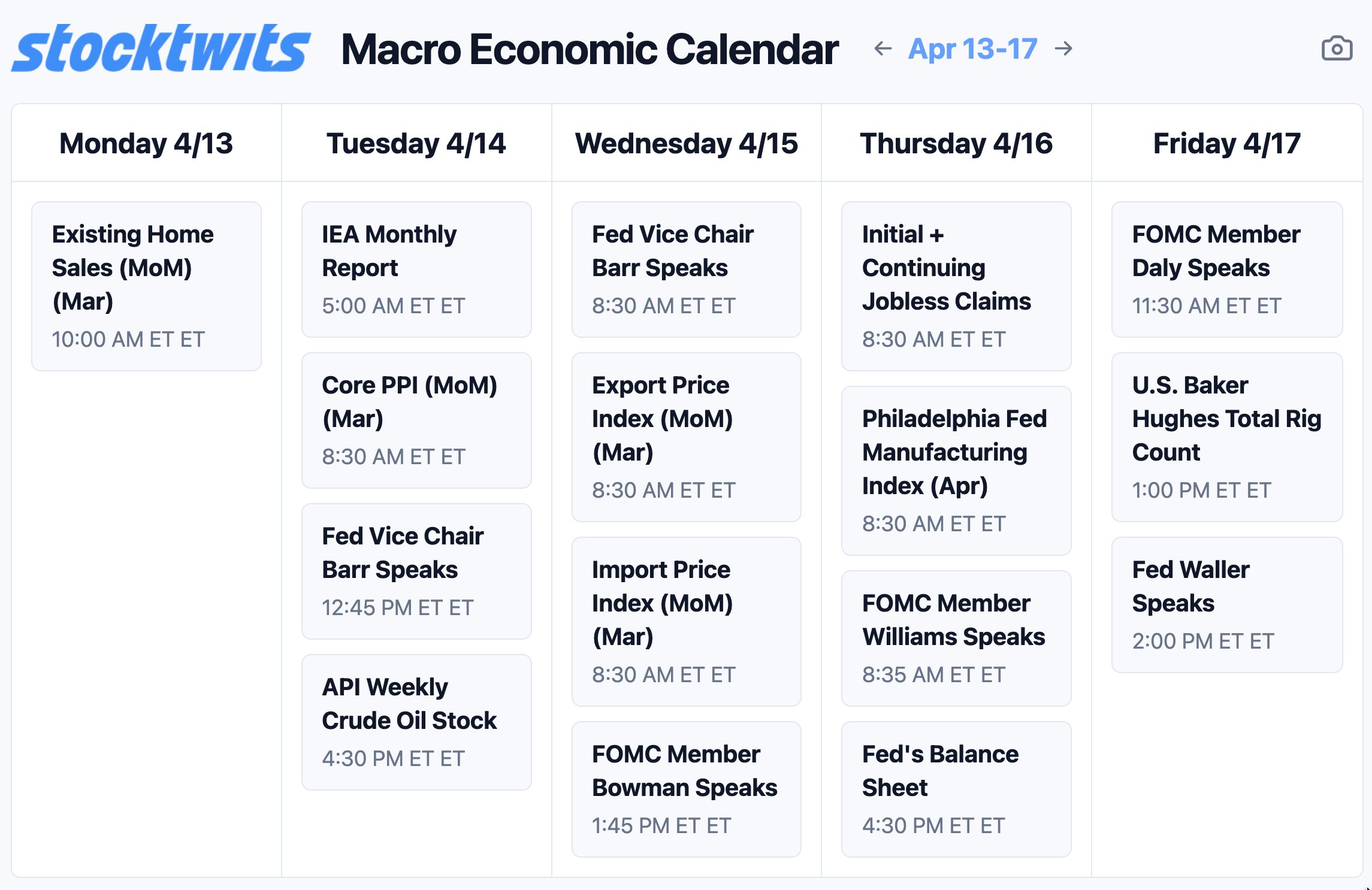

Macro

Mon: Existing Home Sales (MoM) (Mar) (10:00 AM ET)

Tue: IEA Monthly Report (5:00 AM ET), ADP Employment Change Weekly (8:15 AM ET), Core PPI (MoM) (Mar) (8:30 AM ET), Fed Vice Chair Barr Speaks (12:45 PM ET), +1 more

Wed: Fed Vice Chair Barr Speaks (8:30 AM ET), Export Price Index (MoM) (Mar) (8:30 AM ET), Import Price Index (MoM) (Mar) (8:30 AM ET), Cushing Crude Oil Inventories (10:30 AM ET), +3 more

Thu: Initial + Continuing Jobless Claims (8:30 AM ET), Philadelphia Fed Manufacturing Index (Apr) (8:30 AM ET), FOMC Member Williams Speaks (8:35 AM ET), Industrial Production (MoM) (Mar) (9:15 AM ET), +1 more

Fri: FOMC Member Daly Speaks (11:30 AM ET), U.S. Baker Hughes Total Rig Count (1:00 PM ET), Fed Waller Speaks (2:00 PM ET)

THE CASHTAG AWARDS

The BIGGEST night in Finance. May 4th. NYSE.

The Cashtag Awards are built by the Stocktwits community and it wouldn't be the same without you in the room!

We're offering a limited number of fully comped tickets for members who want to show up, represent, and help make this night as special as it should be.

Want to celebrate with us on May 4th?

Links That Don’t Suck 🌐

Get In Touch 📬

How Was The Daily Rip Today?

Terms & Conditions 📝

Securities Disclaimer: STOCKTWITS IS NOT A TAX ADVISOR, BROKER, FINANCIAL ADVISOR OR INVESTMENT ADVISOR. THE SERVICE IS NOT INTENDED TO PROVIDE TAX, LEGAL, FINANCIAL OR INVESTMENT ADVICE, AND NOTHING ON THE SERVICE SHOULD BE CONSTRUED AS AN OFFER TO SELL, A SOLICITATION OF AN OFFER TO BUY, OR A RECOMMENDATION FOR ANY SECURITY. Trading in such securities can result in immediate and substantial losses of the capital invested. You should only invest risk capital, and not capital required for other purposes. You alone are solely responsible for determining whether any investment, security or strategy, or any other product or service, is appropriate or suitable for you based on your investment objectives and personal and financial situation. You should also consult an attorney or tax professional regarding your specific legal or tax situation. The Content is to be used for informational and entertainment purposes only and the Service does not provide investment advice for any individual. Stocktwits, its affiliates and partners specifically disclaim any and all liability or loss arising out of any action taken in reliance on Content, including but not limited to market value or other loss on the sale or purchase of any company, property, product, service, security, instrument, or any other matter. You understand that an investment in any security is subject to a number of risks, and that discussions of any security published on the Service will not contain a list or description of relevant risk factors. In addition, please note that some of the stocks about which Content is published on the Service have a low market capitalization and/or insufficient public float. Such stocks are subject to more risk than stocks of larger companies, including greater volatility, lower liquidity and less publicly available information. Read the full terms & conditions here. 🔍

Author Disclosure: The author of this newsletter does not hold positions in any of the securities or assets mentioned. 📋