The Weekend Rip

Happy Weekend!

U.S. markets navigated a chaotic mid-term election year kickoff, swinging from a DOJ investigation into Fed Chair Powell and 10% credit card rate cap threats to a massive AI-fueled recovery. While big tech and utilities were jolted by Trump’s "emergency power auctions" and "physical AI" demands, Taiwan Semi’s record $56 billion CapEx and Meta’s nuclear energy deals proved the infrastructure boom is far from over. The week culminated in a record-breaking surge for small caps, leaving investors to balance a high-stakes geopolitical landscape involving Venezuela and Greenland against a historic wave of upcoming mega-IPOs and corporate restructuring.

Let's recap and prep you for the week ahead. 📝

Monday 📉: The market kicked off the week under a cloud of "Fed noise" as the DOJ launched a criminal investigation into Chair Jerome Powell over headquarters renovation costs, a move Powell slammed as political retaliation for the Fed's independence. Trump further shook the tape by teasing a 10% interest rate cap on credit cards, kneecapping consumer lenders like AmEx and Capital One ahead of their earnings. Despite the drama, Alibaba surged 10% after its Qwen AI models hit 700 million downloads, while Walmart prepared to join the Nasdaq-100 on January 20th as part of its ongoing pivot into a tech-forward retailer.

Tuesday 🐌 : The market limped through the official start of earnings season as JPMorgan and Delta both fell despite beating profit estimates, with investors spooked by soft revenue guidance and a $2.2 billion loan-loss reserve for the Apple Card. Software stocks like Adobe and Salesforce were "taken to the woodshed," dropping 5% after Oppenheimer warned that AI tools aren't boosting sales fast enough to justify high valuations. Meanwhile, the Department of War made a historic $1 billion equity investment in L3Harris to secure the "Arsenal of Freedom," while Trump sent tech giants into a tailspin by demanding they pay for their own data center power to lower electricity bills for average Americans.

⚡ On Wednesday: The S&P 500 fell away from the 7,000 mark as a "mixed" banking earnings season and hot 3.0% PPI data cooled rate-cut hopes, while Trump’s threat to cap credit card interest rates sent big bank stocks sliding 5% alongside high earnings expectations. Geopolitical tension reached a boiling point as the U.S. declared any outcome less than control of Greenland "unacceptable" and evacuations began in Qatar amid reports of up to 2,000 deaths in the ongoing Iranian internet blackout. Meanwhile, Netflix prepared a "sweetened" all-cash bid to accelerate its $82.7 billion takeover of Warner Bros. Discovery as bidders scramble to finalize plans.

Thursday 🏦: Markets bounced back as a triple-threat of bank beats and a massive 35% profit surge from Taiwan Semi restored confidence in the AI "supercycle." TSMC’s record-breaking $56 billion CapEx forecast for 2026 ignited a sector-wide rally, while the U.S. dropped Taiwan's tariffs to 15% in exchange for a massive $250 billion investment pledge. Between BlackRock hitting a historic $14 trillion in assets and Trump unveiling "The Great Healthcare Plan" to bypass insurance middle-men, the day was defined by high-stakes policy shifts and the return of "big bank" swagger.

Friday 🎅: Small caps led the way as the Russell 2000 hit a record high, even as blue chips limped into the holiday weekend following Trump’s decision to keep Kevin Hassett away from the Fed chairmanship. ImmunityBio skyrocketed 38% on triple-threat clinical wins, while nuclear darlings Vistra and Constellation Energy tanked after the administration proposed an "emergency power auction" to force Big Tech to subsidize household electricity. Meanwhile, regional banks delivered a mixed bag of earnings, with PNC crushing estimates while State Street slid on repositioning charges, leaving investors to weigh record-high small-cap momentum against a fresh "power shock" to the utility sector.

🤩 This week's Stocktwits Top 25 showed outperformance vs. the indexes.

Here are the closing prices:

THE BRIEF

Need a concise summary of what's going on this week? Look no further. Here’s a rundown of this week’s earnings and economic data.

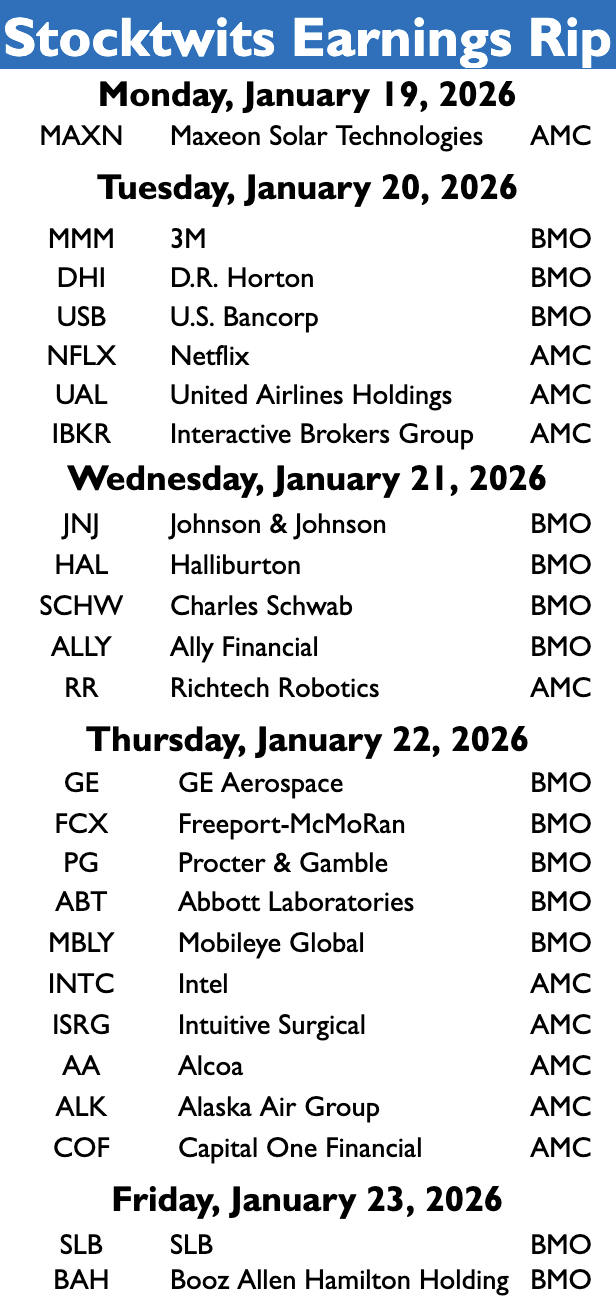

Earnings This Week

Above is a quick summary. Check out the full Stocktwits earnings calendar for the other names reporting this week.

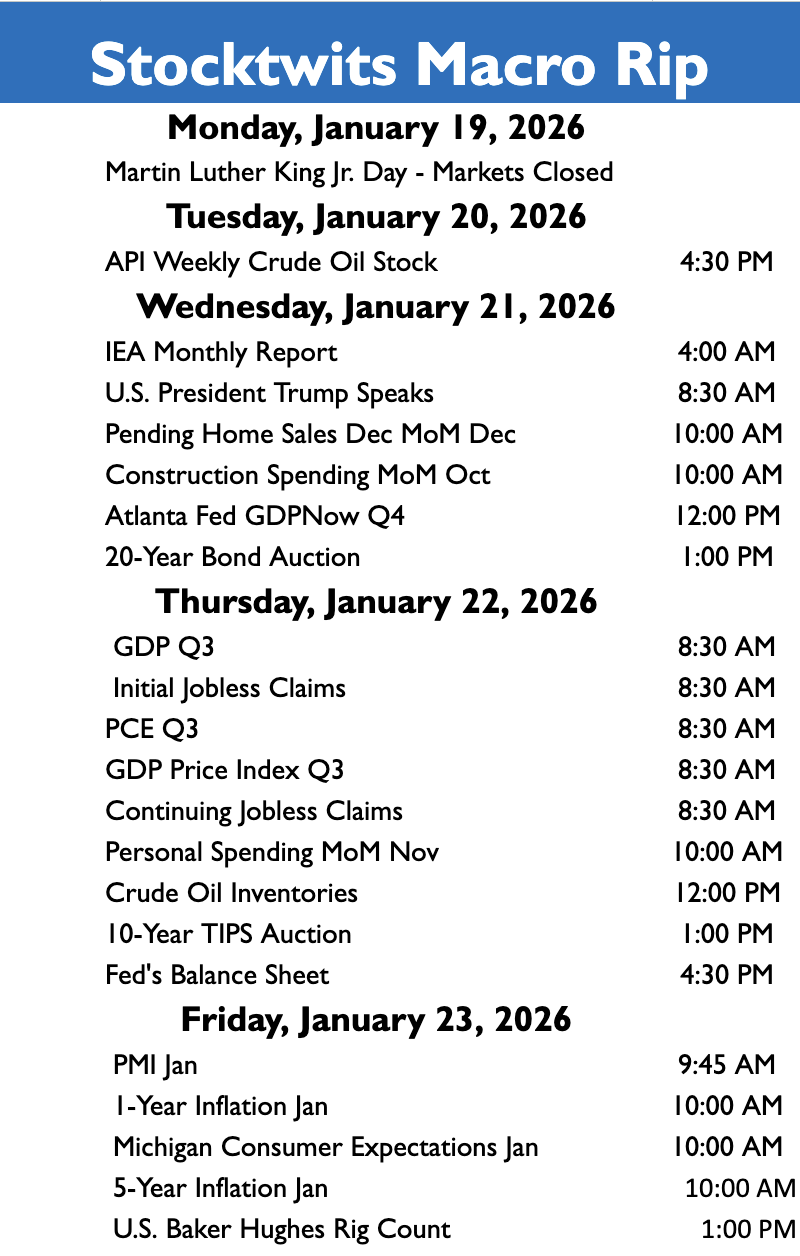

Economic Calendar

In addition to the above, check out this week's complete list of economic releases.

Links That Don’t Suck 🌐

⚠ Trump in Davos, Netflix and Intel results on deck as earnings season ramps: What to watch this week

*3rd Party Ad. Not an offer or recommendation by Stocktwits. See disclosure here.

Get In Touch 📬

How Was The Daily Rip Today?

Terms & Conditions 📝

Securities Disclaimer: STOCKTWITS IS NOT A TAX ADVISOR, BROKER, FINANCIAL ADVISOR OR INVESTMENT ADVISOR. THE SERVICE IS NOT INTENDED TO PROVIDE TAX, LEGAL, FINANCIAL OR INVESTMENT ADVICE, AND NOTHING ON THE SERVICE SHOULD BE CONSTRUED AS AN OFFER TO SELL, A SOLICITATION OF AN OFFER TO BUY, OR A RECOMMENDATION FOR ANY SECURITY. Trading in such securities can result in immediate and substantial losses of the capital invested. You should only invest risk capital, and not capital required for other purposes. You alone are solely responsible for determining whether any investment, security or strategy, or any other product or service, is appropriate or suitable for you based on your investment objectives and personal and financial situation. You should also consult an attorney or tax professional regarding your specific legal or tax situation. The Content is to be used for informational and entertainment purposes only and the Service does not provide investment advice for any individual. Stocktwits, its affiliates and partners specifically disclaim any and all liability or loss arising out of any action taken in reliance on Content, including but not limited to market value or other loss on the sale or purchase of any company, property, product, service, security, instrument, or any other matter. You understand that an investment in any security is subject to a number of risks, and that discussions of any security published on the Service will not contain a list or description of relevant risk factors. In addition, please note that some of the stocks about which Content is published on the Service have a low market capitalization and/or insufficient public float. Such stocks are subject to more risk than stocks of larger companies, including greater volatility, lower liquidity and less publicly available information. Read the full terms & conditions here. 🔍

Author Disclosure: The author of this newsletter does not hold positions in any of the securities or assets mentioned. 📋