The Weekend Rip

Happy Weekend!

Stocks spent the week trying to outrun inflation, oil, and rates with AI duct tape. Monday and Tuesday were all crude and CPI stress, Wednesday brought hot PPI and another Nasdaq record, Thursday turned into an AI-China roadshow, and Friday finally let yields punch the tape in the mouth. Underneath it all, the market’s favorite question stayed the same: is this broadening, or just the same AI trade with a passport, a higher multiple, and worse bond math?

Let's recap and prep you for the week ahead. 📝

Monday 🛢️: Stocks closed green, but the leadership was anything but broad. Oil jumped on renewed Iran risk, AI infrastructure names ripped, and classic defensives cracked while traders looked ahead to CPI.

Tuesday 🧾: Stocks slipped as hot CPI and $102 crude dragged tech lower, even as the Dow finished green. The day’s tape was a clean rotation out of Monday’s chip winners and into inflation-defense mode.

Wednesday 🔥: Stocks gained ground while producer prices came in scorching hot, which is the market equivalent of hearing the smoke alarm and turning the music up. The Nasdaq pushed to another record as AI, China, and earnings kept traders busy, with Cisco and Alibaba both giving investors something to argue about. Warsh got confirmed at the Fed, Iran risk kept inflation pressure in the frame, and rate-cut hopes looked like they needed a long walk.

Thursday 🌏: Stocks climbed as the AI trade grabbed its passport, with tech leading while Trump, Xi, Nvidia, and the CEO roadshow gave traders plenty to chew on. Figma delivered the clean after-hours SaaS beat, Rumble tried to sell an AI infrastructure reset through an earnings miss, and Cerebras gave IPO watchers a full-blown inference-chip face-ripper. Under the hood, the market still had one big question: is AI broadening, or is everyone just paying more for the same theme?

Friday 🧨: Stocks cooled off after the record run as the China trip failed to deliver the chip thaw traders wanted and yields finally started bossing equities around. The 30-year Treasury topped 5.1%, hot inflation data kept the Fed-hike trade alive, and AI leaders lost altitude. Stocktwits still had mega-cap attention on Nvidia and silver, but the real post-level heat came from POET financing drama and Candel’s prostate cancer data.

🤩 This week's Stocktwits Top 25 showed how momentum movers fared vs. the indexes.

Here are the closing prices:

THE BRIEF

Need a concise summary of what's going on this week? Look no further. Here’s a rundown of this week’s earnings and economic data.

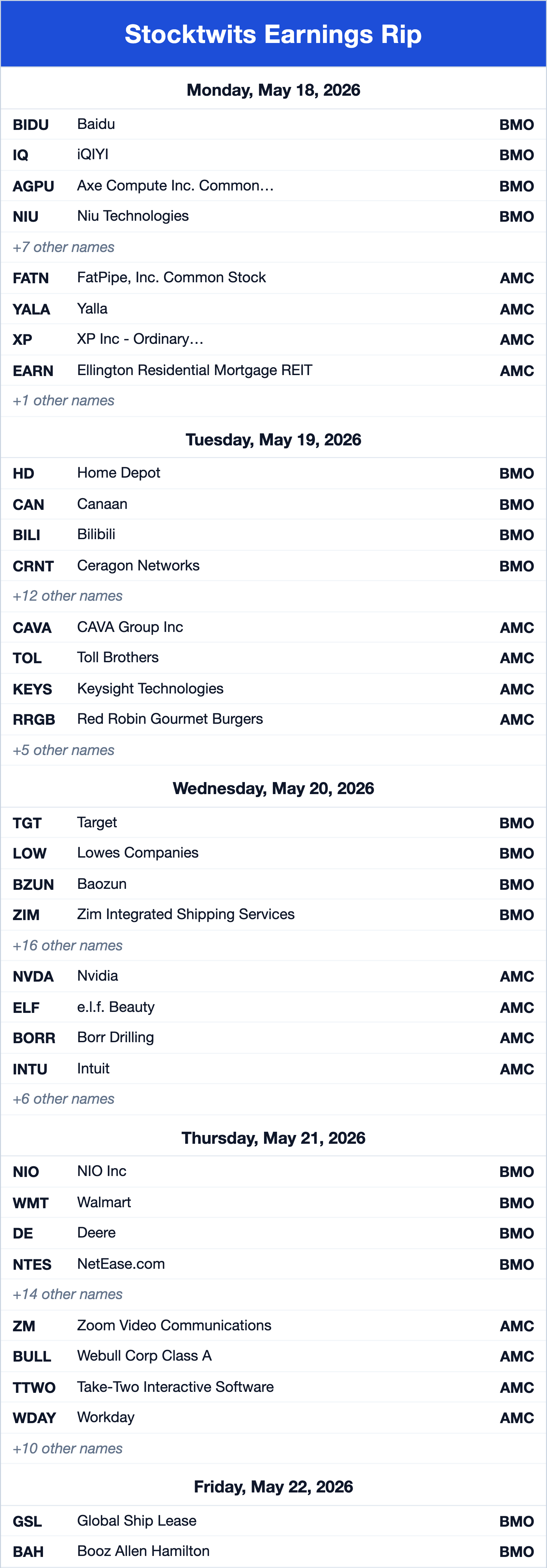

Earnings This Week

Above is a quick summary. Check out the full Stocktwits earnings calendar for the other names reporting this week.

Economic Calendar

In addition to the above, check out this week's complete list of economic releases.

ST EDITOR’S PICKS

Links That Don’t Suck 🌐

🆘 Get data-driven investing insights and our biggest IBD Digital discount of the year––over $200 off*

*3rd Party Ad. Not an offer or recommendation by Stocktwits. See disclosure here.

Get In Touch 📬

How Was The Daily Rip Today?

Terms & Conditions 📝

Securities Disclaimer: STOCKTWITS IS NOT A TAX ADVISOR, BROKER, FINANCIAL ADVISOR OR INVESTMENT ADVISOR. THE SERVICE IS NOT INTENDED TO PROVIDE TAX, LEGAL, FINANCIAL OR INVESTMENT ADVICE, AND NOTHING ON THE SERVICE SHOULD BE CONSTRUED AS AN OFFER TO SELL, A SOLICITATION OF AN OFFER TO BUY, OR A RECOMMENDATION FOR ANY SECURITY. Trading in such securities can result in immediate and substantial losses of the capital invested. You should only invest risk capital, and not capital required for other purposes. You alone are solely responsible for determining whether any investment, security or strategy, or any other product or service, is appropriate or suitable for you based on your investment objectives and personal and financial situation. You should also consult an attorney or tax professional regarding your specific legal or tax situation. The Content is to be used for informational and entertainment purposes only and the Service does not provide investment advice for any individual. Stocktwits, its affiliates and partners specifically disclaim any and all liability or loss arising out of any action taken in reliance on Content, including but not limited to market value or other loss on the sale or purchase of any company, property, product, service, security, instrument, or any other matter. You understand that an investment in any security is subject to a number of risks, and that discussions of any security published on the Service will not contain a list or description of relevant risk factors. In addition, please note that some of the stocks about which Content is published on the Service have a low market capitalization and/or insufficient public float. Such stocks are subject to more risk than stocks of larger companies, including greater volatility, lower liquidity and less publicly available information. Read the full terms & conditions here. 🔍

Author Disclosure: The author of this newsletter does not hold positions in any of the securities or assets mentioned. 📋