Presented by

The Weekend Rip

Happy Weekend!

U.S. markets kicked off 2026 with a high-stakes blend of "Delta Force diplomacy" in Venezuela and a massive tech-driven infrastructure boom that sent the S&P 500 and Dow to fresh all-time highs. The Russell 2000 made outside gains though, the tech market finally broadening out. The Mag 7 was not far behind Meta’s historic 6.6 GW nuclear energy deals, showing investors still spent the week betting on a future powered by American commodities and an insatiable AI "storage supercycle." 📉

Let's recap and prep you for the week ahead. 📝

Monday 🍏 The new year roared green as markets embraced "Delta Force diplomacy" following the U.S. capture of Nicolas Maduro, sending oil services stocks like Halliburton and SLB soaring on hopes of a $100 billion Venezuelan infrastructure rebuild. While the S&P 500 officially triggered a "failed Santa Rally" warning with a lackluster seven-day return, Nvidia’s Jensen Huang stole the spotlight at CES by unveiling the "Vera Rubin" supercomputing system and a "human-like" autonomous driving model. Between Maduro pleading not guilty in a New York courthouse and the Monroe Doctrine trending on Wall Street, the week began with a massive bet that American "boots on the ground" will eventually lead to cheaper barrels.

Tuesday 🐌 : The S&P 500 and Dow hit fresh records as a storage "supercycle" took hold, with SanDisk skyrocketing 27% and Western Digital climbing 16% after Nvidia’s CEO identified memory as a massive unserved market. Trump’s priority on acquiring Greenland sent rare earth miner Critical Materials flying 25%, while crypto giants like MicroStrategy slumped after MSCI officially excluded bitcoin treasuries from its indexes. Between Elon Musk’s xAI closing a $20 billion round and a flurry of breakthroughs in nuclear energy and biotech, the market chose to ignore a weak Services PMI in favor of a full-scale AI infrastructure boom.

⚡ On Wednesday, the S&P 500 pulled back from the 7,000 level as weak labor data from ADP and JOLTS signaled a four-year high in unemployment, cooling the recent tech-fueled optimism. Geopolitics dominated the tape as Trump announced the U.S. will indefinitely control Venezuelan oil exports, while his threats to cap executive pay at defense giants like Lockheed and RTX sent sector shares tumbling 5%. Meanwhile, the "Year of the Mega-IPO" kicked off with Discord filing for a $15 billion debut, and housing stocks like Blackstone and Invitation Homes slid after the President vowed to ban corporate ownership of single-family homes to address the cost-of-living crisis.

Thursday 🐔: Tech stocks pulled back as the market wrestled with a flurry of headlines, including a narrowed U.S. trade deficit and a looming Supreme Court decision on the legality of Trump’s tariffs. China stocks caught fire on reports that Beijing will approve massive Nvidia H200 buying, while Tilray Brands jumped 7% after-hours on record medical cannabis revenue. In a whirlwind of "Tweet Train" policy, the President pivoted from banning institutional landlords to directing a $200 billion government buy of mortgage bonds, while defense giants recovered on his proposed $1.5 trillion budget. The country endured a tragedy in Minnesota. Meanwhile, silver surged past $75 on industrial AI demand, even as paper futures saw extreme volatility from institutional rebalancing.

Friday ☢️: The stock market "went nuclear" to end the week as Meta sparked a massive sector rally with landmark deals to secure 6.6 GW of carbon-free power from Oklo, TerraPower, and Vistra. Small-caps finally broke out to all-time highs, signaling broad market support even as the Supreme Court punted its decision on the legality of Trump’s tariffs to next Wednesday. While a soft December jobs report (just 50k added) boosted rate-cut odds, residential real estate stocks like Opendoor surged 20% on the President’s $200 billion mortgage bond push. The week closed on a high note with Merck reportedly nearing a $30 billion acquisition of Revolution Medicines, solidifying 2026's start as a year of high-stakes infrastructure and massive M&A.

🤩 This week's Stocktwits Top 25 showed outperformance vs. the indexes.

Here are the closing prices:

SPONSORED BY ZENATECH

ZenaTech Completes 20th Acquisition in Year One of Drone as a Service

ZenaTech recently announced it has completed its 20th acquisition with the addition of L.D. King, Inc., a well-established civil engineering and land surveying firm based in the Los Angeles area. The acquisition strengthens ZenaTech’s drone solutions footprint in one of the most wildfire-sensitive and disaster-prone regions in the US and marks a successful first year executing its Drone as a Service expansion strategy. Since January 2025, the company has built a US and global business network with thousands of commercial and government client relationships.

Founded in 1965, L.D. King has served Southern California for more than six decades, with a strong reputation across public works, commercial, and residential projects. Its licensed professionals provide land surveying, engineering, planning, and construction management services to public agencies and private developers.

For complete ZenaTech disclaimers and disclosures, please visit ZenaTech here.

*3rd Party Ad. Not an offer or recommendation by Stocktwits. See disclosure here.

THE BRIEF

Need a concise summary of what's going on this week? Look no further. Here’s a rundown of this week’s earnings and economic data.

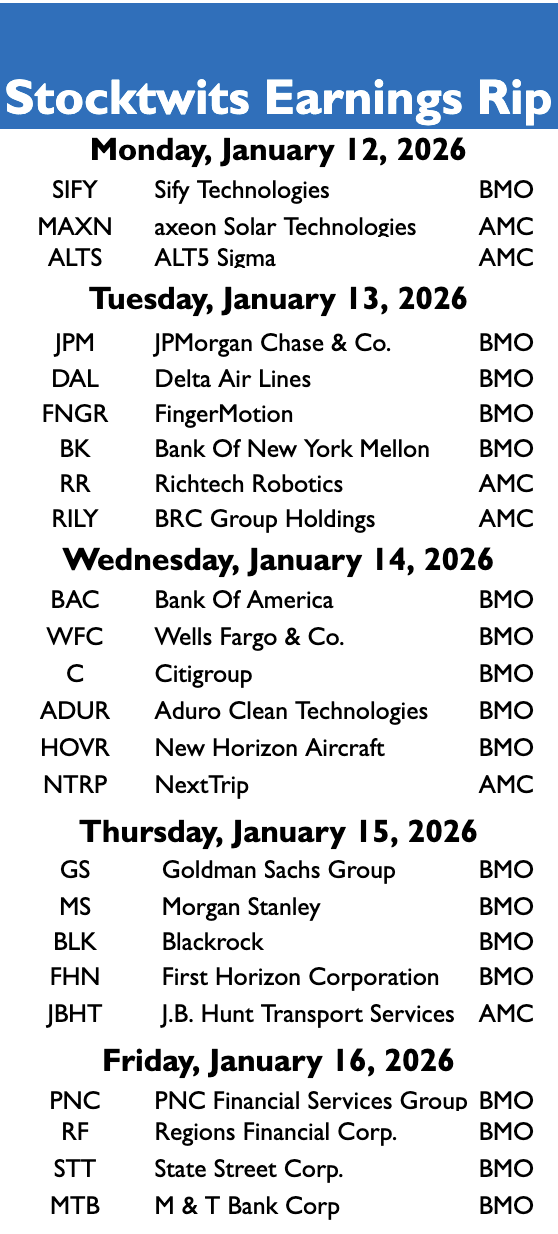

Earnings This Week

Above is a quick summary. Check out the full Stocktwits earnings calendar for the other names reporting this week.

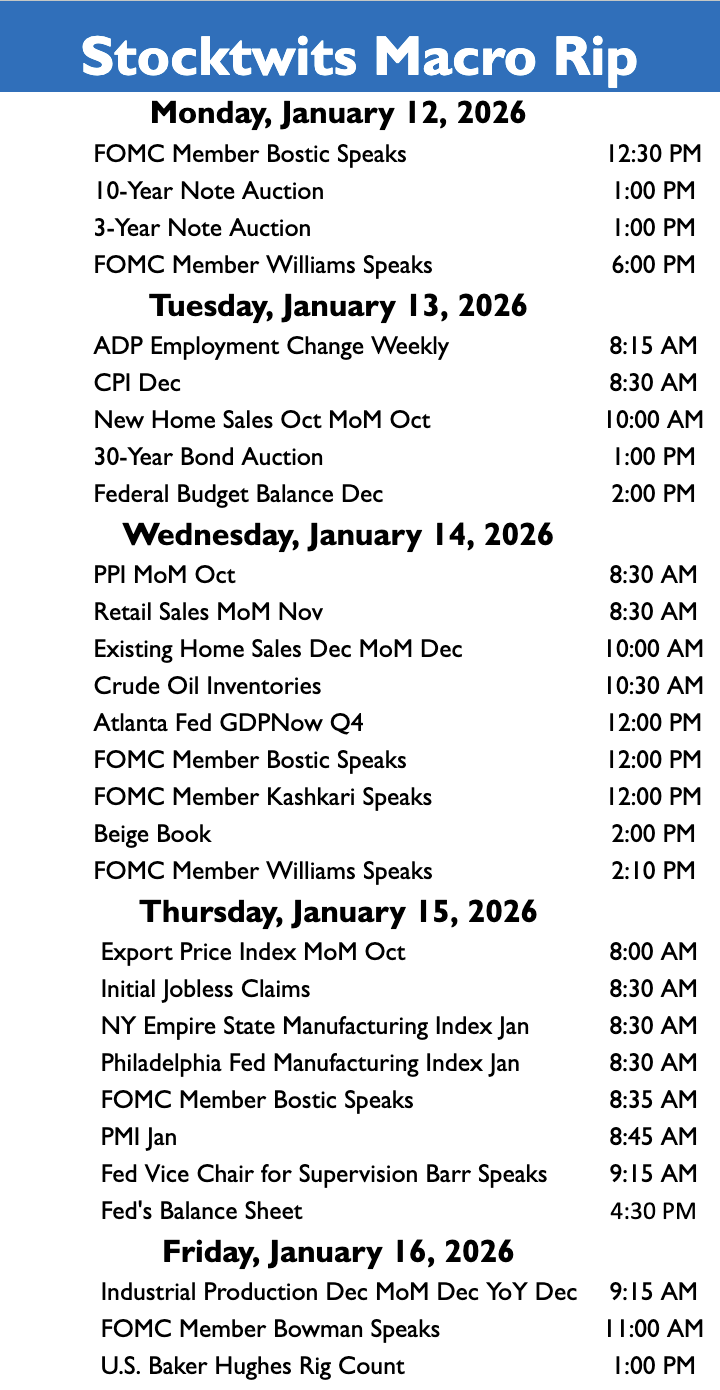

Economic Calendar

In addition to the above, check out this week's complete list of economic releases.

Links That Don’t Suck 🌐

🤑 Big banks kick off fourth quarter earnings season, inflation data on deck: What to watch this week

*3rd Party Ad. Not an offer or recommendation by Stocktwits. See disclosure here.

Get In Touch 📬

How Was The Daily Rip Today?

Terms & Conditions 📝

Securities Disclaimer: STOCKTWITS IS NOT A TAX ADVISOR, BROKER, FINANCIAL ADVISOR OR INVESTMENT ADVISOR. THE SERVICE IS NOT INTENDED TO PROVIDE TAX, LEGAL, FINANCIAL OR INVESTMENT ADVICE, AND NOTHING ON THE SERVICE SHOULD BE CONSTRUED AS AN OFFER TO SELL, A SOLICITATION OF AN OFFER TO BUY, OR A RECOMMENDATION FOR ANY SECURITY. Trading in such securities can result in immediate and substantial losses of the capital invested. You should only invest risk capital, and not capital required for other purposes. You alone are solely responsible for determining whether any investment, security or strategy, or any other product or service, is appropriate or suitable for you based on your investment objectives and personal and financial situation. You should also consult an attorney or tax professional regarding your specific legal or tax situation. The Content is to be used for informational and entertainment purposes only and the Service does not provide investment advice for any individual. Stocktwits, its affiliates and partners specifically disclaim any and all liability or loss arising out of any action taken in reliance on Content, including but not limited to market value or other loss on the sale or purchase of any company, property, product, service, security, instrument, or any other matter. You understand that an investment in any security is subject to a number of risks, and that discussions of any security published on the Service will not contain a list or description of relevant risk factors. In addition, please note that some of the stocks about which Content is published on the Service have a low market capitalization and/or insufficient public float. Such stocks are subject to more risk than stocks of larger companies, including greater volatility, lower liquidity and less publicly available information. Read the full terms & conditions here. 🔍

Author Disclosure: The author of this newsletter does not hold positions in any of the securities or assets mentioned. 📋