Presented by

The Weekend Rip

Happy Weekend!

The market successfully survived a "hiring recession" and a government shutdown this quarter to deliver the beginning trades of a classic Santa Rally, capped off by record-breaking runs in gold and silver. From Larry Ellison’s $40 billion backing of PSKY’s WBD offer, to Nvidia’s $20 billion Groq "partnership," the week was defined by massive capital and low volume. Looking ahead, expect low-volume trading and potential fireworks from Tuesday’s FOMC minutes as investors try to figure out if the 2026 outlook is actually "flush" or just a high-tariff AI hallucination.

Let's recap and prep you for the week ahead. 📝

Monday 📉 : The market kicked off the week in a green "Santa Rally" warmup as Google dropped $4.75 billion on solar fields to fuel its AI tentacles and Tesla hit yet another record. Larry Ellison tried to end the Paramount-WBD soap opera by personally guaranteeing $40 billion for his son's hostile bid, while Disney finally kissed and made up with patent-holder Adeia to keep its streaming lights on. Between seized Venezuelan oil tankers and a French fry shortage at McDonald’s, investors found refuge in gold and silver as the "most wonderful time of the year" felt more like a billion-dollar shopping spree for energy and IP.

Tuesday 🥇: The market hit record highs on a massive 4.3% GDP growth beat, though skeptics noted the gains were fueled by century-high tariffs and a "K-shaped" economy where only the rich are still vibing. ServiceNow dropped $7.75 billion on a security deal to become an "AI Control Tower," while Novo Nordisk jumped 8% after the FDA approved a weight-loss pill for those of us who prefer "fat pills" over needles. Meanwhile, silver and gold smashed through historic ceilings, proving that even in a digital age, investors still want to hoard shiny metal like it’s 1849.

Wednesday 🎅: The Santa Rally officially kicked off during a sleepy half-day of trade, with the S&P 500 hitting fresh highs while trading volume was so low you'd think the floor traders all left early for eggnog. Dynavax skyrocketed 38% on a $2.2 billion buyout from Sanofi, and biotech peer Omeros flew 75% after the FDA handed out an early Christmas gift in the form of a rare drug approval. While AI-crazed tech and silver dominated the year's leaderboard, the "bond proxies" in the Utilities sector ended 2025 as the ultimate lumps of coal for investors.

Thursday, the market was closed for Christmas.

Friday 💫 : The market drifted through a low-volume Christmas hangover as gold and silver smashed fresh records, proving that investors currently trust shiny metal more than the "noisy" economy. Nvidia dominated the headlines with a $20 billion "acquisition-lite" of AI startup Groq, while Target found itself in the crosshairs of an activist investor. Between Zelenskyy prepping for a Sunday meeting with Trump and the DOJ needing "a few more weeks" to dump the Epstein files, the week ended with a classic mix of holiday optimism and lingering dread.

🤩 This week's Stocktwits Top 25 showed outperformance vs. the indexes.

SPONSORED

Next-Gen Chips, Next-Level Trades

From AI to cleaner energy to faster connectivity, the semiconductor companies driving the next generation of chips are pushing innovation to new frontiers.

Traders bullish on semis use Tradr ETFs to seek 200% daily leverage on four big names – without the complexity of margin accounts or options strategies:

Tradr 2X Long ALAB Daily ETF (Cboe: LABX) – targets Astera Labs (ALAB), a high-speed connectivity solutions company.

Tradr 2X Long LRCX Daily ETF (Cboe: LRCU) – targets Lam Research (LRCX), supplier of wafer fabrication equipment.

Tradr 2X Long NVTS Daily ETF (Cboe: NVTX) – targets Navitas Semiconductor (NVTS), leader in gallium nitride and silicon carbide power chips.

Tradr 2X Long CRDO Daily ETF (Cboe: CRDU) – targets Credo Technology (CRDO), a developer of high-speed connectivity for data centers and cloud computing.

Try Tradr for amplified exposure on ALAB, LRCX, NVTS or CRDO.

Disclaimer: Visit the Tradr ETFs website for an explanation of leveraged ETFs and their significant risks. www.tradretfs.com.

*3rd Party Ad. Not an offer or recommendation by Stocktwits. See disclosure here.

THE BRIEF

Need a concise summary of what's going on this week? Look no further. Here’s a rundown of this week’s earnings and economic data.

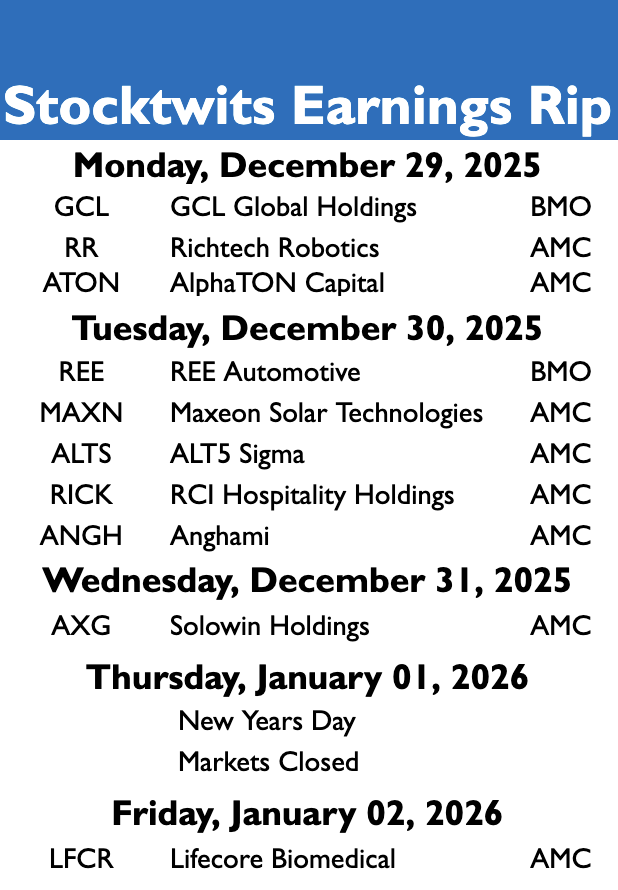

Earnings This Week

Above is a quick summary. Check out the full Stocktwits earnings calendar for the other names reporting this week.

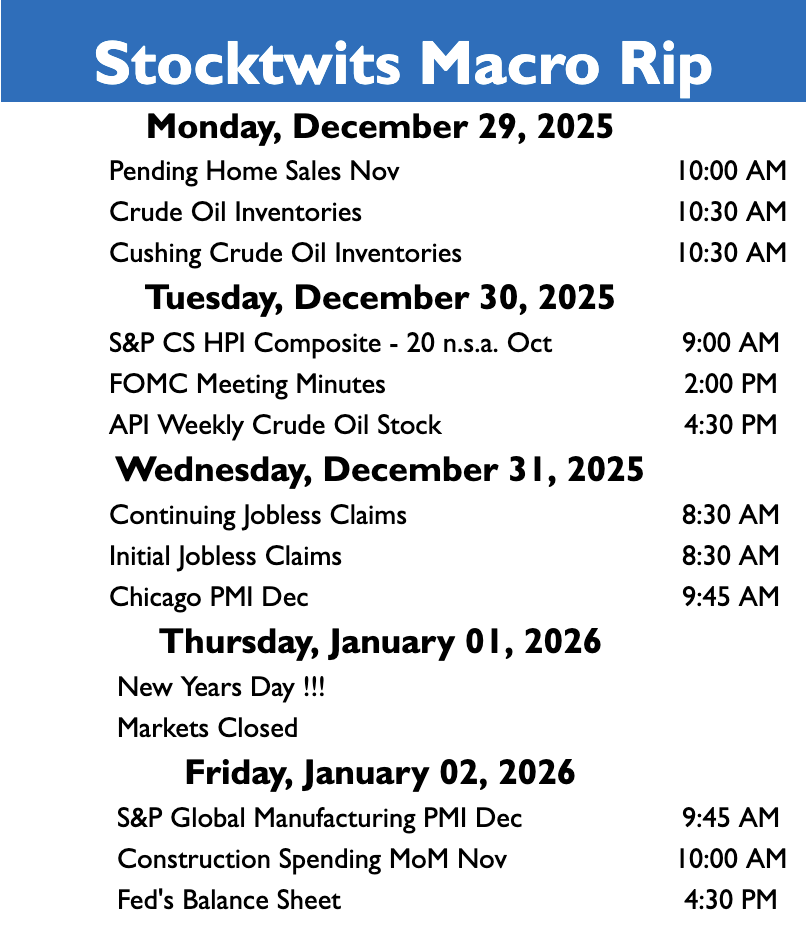

Economic Calendar

In addition to the above, check out this week's complete list of economic releases.

Links That Don’t Suck 🌐

🤑 Stocks sit near record highs as 'Santa Claus rally' builds, 2026 approaches: What to watch this week

*3rd Party Ad. Not an offer or recommendation by Stocktwits. See disclosure here.

Get In Touch 📬

How Was The Daily Rip Today?

Terms & Conditions 📝

Securities Disclaimer: STOCKTWITS IS NOT A TAX ADVISOR, BROKER, FINANCIAL ADVISOR OR INVESTMENT ADVISOR. THE SERVICE IS NOT INTENDED TO PROVIDE TAX, LEGAL, FINANCIAL OR INVESTMENT ADVICE, AND NOTHING ON THE SERVICE SHOULD BE CONSTRUED AS AN OFFER TO SELL, A SOLICITATION OF AN OFFER TO BUY, OR A RECOMMENDATION FOR ANY SECURITY. Trading in such securities can result in immediate and substantial losses of the capital invested. You should only invest risk capital, and not capital required for other purposes. You alone are solely responsible for determining whether any investment, security or strategy, or any other product or service, is appropriate or suitable for you based on your investment objectives and personal and financial situation. You should also consult an attorney or tax professional regarding your specific legal or tax situation. The Content is to be used for informational and entertainment purposes only and the Service does not provide investment advice for any individual. Stocktwits, its affiliates and partners specifically disclaim any and all liability or loss arising out of any action taken in reliance on Content, including but not limited to market value or other loss on the sale or purchase of any company, property, product, service, security, instrument, or any other matter. You understand that an investment in any security is subject to a number of risks, and that discussions of any security published on the Service will not contain a list or description of relevant risk factors. In addition, please note that some of the stocks about which Content is published on the Service have a low market capitalization and/or insufficient public float. Such stocks are subject to more risk than stocks of larger companies, including greater volatility, lower liquidity and less publicly available information. Read the full terms & conditions here. 🔍

Author Disclosure: The author of this newsletter does not hold positions in any of the securities or assets mentioned. 📋